Crypto moving across multiple wallet addresses can look alarming, especially when the transfers happen quickly or involve wallets the owner does not recognize. While this activity often raises concerns about theft or hacking, using multiple wallets is actually common in the crypto space.

It is quite common for people to split their funds according to how they plan on spending their coins or tokens – be it for trade, storing, Defi applications, or daily transactions. Splitting money into various wallets, of course, provides added security.

However, for scammers, splitting up crypto is used for the opposite effect to increase the difficulty of tracing transactions and delaying investigations.

Wallet-related scams are also becoming more sophisticated. In 2025, cybersecurity researchers uncovered more than 270 million blockchain “address poisoning” attempts. These scams use fake wallet addresses that closely resemble legitimate ones, leading users to accidentally send funds to the wrong address. The attacks were linked to at least $83.8 million in confirmed losses.

Understanding why crypto moves between wallets can help users better recognize the difference between normal activity and suspicious behavior.

Why People Use Multiple Crypto Wallets

Many new investors don’t know, but using multiple crypto wallets is a standard thing. For many experienced users, it’s a normal procedure to divide assets amongst wallets for safe crypto management.

Various wallets have various functions, such as:

- Long-term storage: Larger amounts are stored in a wallet that is not used for frequent fetching and storing on a platform or application.

- Trading activity: More frequent buying, selling, and transferring crypto with a separate wallet.

- DeFi and dApp Access: Manage exposure by linking lower-balance wallets to decentralized platforms with DeFi and dApps.

- NFTs and Digital Assets: Using separate management strategies for collectibles and primary assets.

- Daily use: Making smaller wallets for everyday payments or transfers.

This separation can help to minimize risk by separating larger holdings from activities that may have a greater risk of exposure.

Several wallets can also enhance privacy and organization. Users can split up funds to better manage their portfolios or to restrict visibility of their holdings, rather than linking everything to one public address.

Security is also a significant contributor to this. Having multiple wallet addresses would be advisable in case one is compromised by phishing, malicious smart contracts, or leaked credentials, as it would make it hard for the attacker to get everything in one go.

This is one reason why discussions around wallet safety often recommend choosing the right type of wallet for different activities rather than relying on a single address for everything. Users looking to improve their wallet setup can also benefit from understanding how different wallets handle storage, access, and security features.

How Multiple Wallets Can Help Protect Against Scams

One of the biggest advantages of using multiple crypto wallets is that it can reduce the impact of scams, phishing attacks, and compromised platforms.

Many crypto scams begin when users connect their primary wallet to an unfamiliar website, approve a malicious smart contract, or unknowingly expose wallet credentials. If all assets are stored in that single wallet, the damage can be significant.

However, separating wallets helps limit that risk. For example, many experienced users keep their main holdings in a wallet that is rarely used for daily activity. Smaller wallets are then used for trading, DeFi platforms, NFT marketplaces, or testing new applications. This creates a layer of separation between high-value assets and higher-risk activity.

Using multiple wallets can also help users:

- reduce exposure to phishing attempts,

- isolate suspicious transactions,

- limit losses if a wallet becomes compromised,

- and monitor unusual activity more easily.

Some users even create temporary wallets specifically for one-time interactions with unfamiliar platforms.

While no setup can eliminate risk, wallet separation is often viewed as a practical way to improve overall crypto security. Instead of placing every asset in a single location, users spread exposure across different wallets and activities, making it harder for one mistake or compromised connection to affect their entire portfolio.

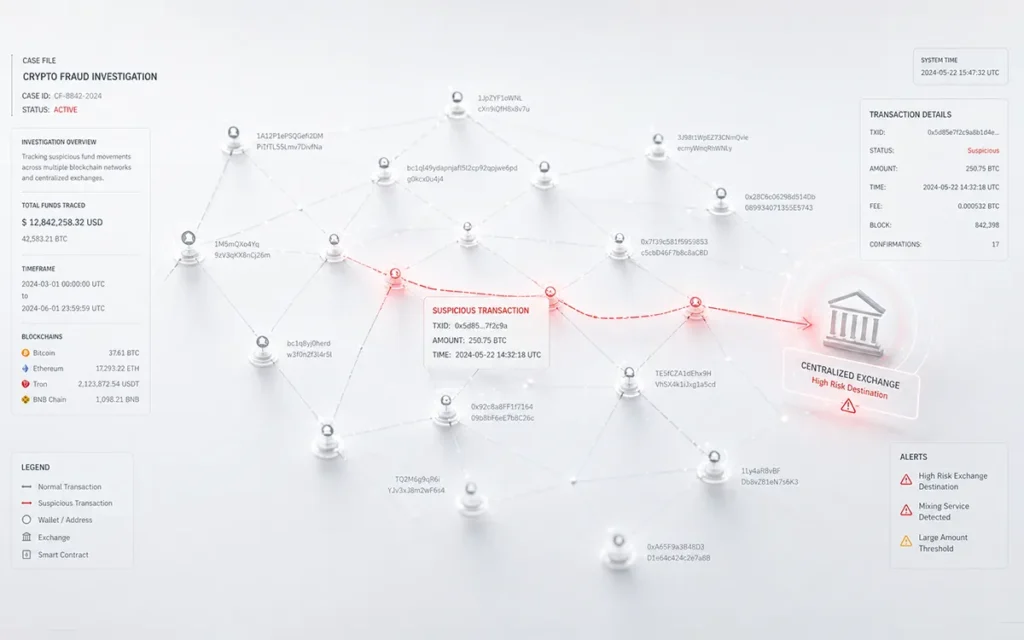

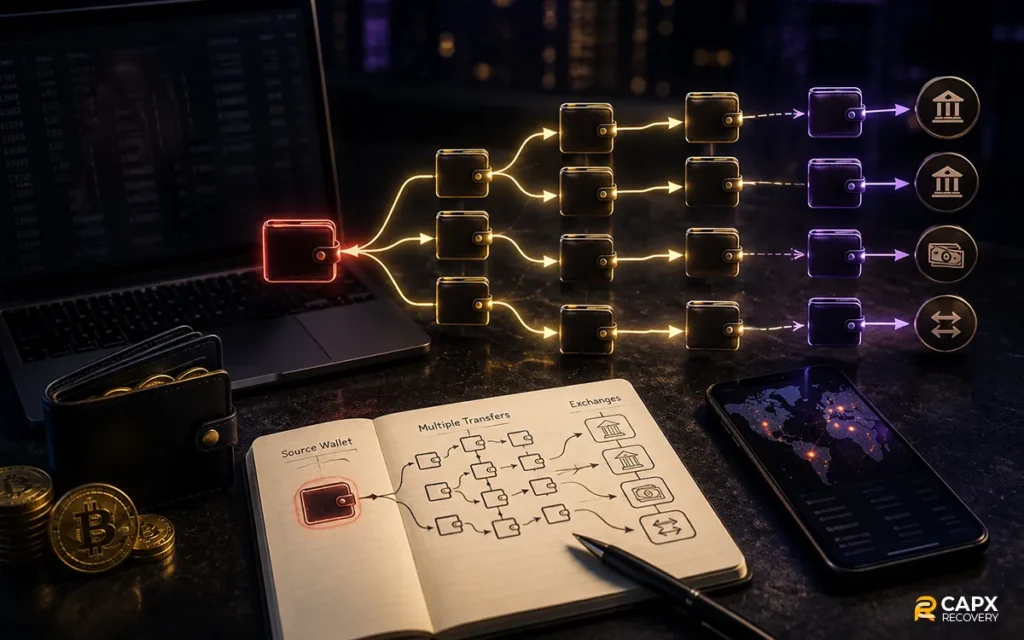

How Scammers Use Multiple Wallet Transfers

While many crypto users rely on multiple wallets for security and organization, scammers often use the same strategy for the opposite reason: making stolen funds harder to trace.

After gaining access to crypto through phishing attacks, fake investment platforms, wallet compromises, or withdrawal scams, scammers rarely leave funds sitting in one address for long. Instead, the crypto is often transferred through multiple wallets in a series of rapid transactions.

Why Scammers Move Crypto Across Multiple Wallets

Moving funds between wallets can help scammers:

- break up visible transaction trails,

- delay investigations,

- make blockchain tracing more complicated,

- and hide connections between wallets.

In some cases, stolen funds are split into smaller amounts and distributed across dozens of addresses before being moved again.

What Victims Usually Notice

For victims, this activity often appears confusing and overwhelming. They may notice:

- repeated transfers between unknown wallet addresses,

- funds suddenly splitting into multiple transactions,

- crypto moving quickly after a deposit,

- or assets disappearing across several wallets within minutes or hours.

This process is sometimes referred to as wallet hopping, layering, or transaction obfuscation, but the goal is usually the same: making it harder to follow where the funds ultimately went.

Multiple Wallet Transfers Do Not Always Mean Fraud

Using multiple wallets is extremely common in crypto. Exchanges, DeFi platforms, traders, and experienced users often separate funds across different wallets for security, privacy, or operational reasons.

The concern usually begins when the transfers are unexpected or tied to other suspicious activity. Users may notice funds moving immediately after a deposit, repeated transfers linked to withdrawal problems, or transaction activity they never approved.

The key difference is context. Legitimate wallet activity is usually expected, authorized, and transparent, while scam-related transfers often appear sudden, unexplained, or connected to restricted account access and withdrawal issues.

What To Do if Your Crypto Was Moved Across Multiple Wallets

If your crypto suddenly starts moving across multiple wallet addresses without your approval, it is important to act quickly and stay organized. Scammers often move stolen funds rapidly to create confusion and complicate blockchain tracing efforts. Taking the right steps early can help preserve evidence and improve visibility into where the assets were transferred.

Stop Interacting With Suspicious Platforms

If you are aware of a fraudulent situation, do not send extra money or send further messages to the platform, recovery agent, or investment manager asking them to send more money. Withdrawal scam recovery cases often end up with the scammer demanding more to be deposited, verified with a payment, or paid in taxes prior to when contact is lost.

Save Transaction Hashes and Wallet Addresses

Documenting wallet activity as early as possible can become extremely important during a blockchain investigation. Save transaction hashes, wallet addresses, screenshots, platform URLs, account balances, and any conversations connected to the incident. These records may help establish transaction timelines and track the movement of funds across wallets.

Review Wallet Permissions

If you connected your wallet to a DeFi application or signed transactions on an unfamiliar platform, review your wallet permissions carefully. Some scams rely on malicious smart contract approvals that continue allowing access to wallet assets even after the original transaction is completed.

Readers unfamiliar with these scams can learn more in this guide on DeFi Wallet Scams Guide.

Revoke Suspicious Smart Contract Access

Once you have reviewed the wallet permissions, remove access to any contracts or applications that you don’t recognize or trust. The elimination of unnecessary approvals may help mitigate the possibility of further unauthorized transfers and the ability of scammers to continue accessing wallet assets.

Contact Exchanges if Applicable

If any wallet addresses involved belong to a centralized exchange, contacting the exchange quickly may help flag suspicious activity. Some exchanges cooperate with fraud investigations and may review accounts connected to reported transactions when sufficient evidence is provided.

Use Blockchain Tracing Tools

Because blockchain transactions are publicly recorded, users can often follow wallet movements using blockchain explorers and crypto tracing tools. This process may help identify connected wallet addresses, exchange deposits, cross-chain transfers, or additional transaction patterns linked to the scam.

For a deeper explanation of how crypto tracing works, see: Cryptocurrency Forensics Explained

Seek Professional Tracing Support if Needed

In more complex cases, victims may collaborate with blockchain investigation experts to delve deeper into the transactional activity. A professional crypto tracing service can be beneficial in organizing wallet data, tracing the flow of funds, and preparing documentation that can assist in reporting to the exchanges or law enforcement agencies.

While tracing stolen crypto does not guarantee recovery, acting quickly and preserving accurate records can significantly improve the chances of understanding where the funds ultimately moved.

How To Use Multiple Wallets Safely

Using multiple wallets can improve both security and organization when managed properly. Many crypto users separate wallets based on purpose, reducing the risk that one compromised platform or transaction affects all of their assets.

- Keep Separate Wallets for Trading and Storage

Many users keep one wallet for daily trading and another for long-term storage. This helps limit exposure if a trading platform or connected application becomes compromised.

- Use Hardware Wallets for Large Balances

Hardware wallets store private keys offline, making them a common choice for secure crypto storage. They are often used to protect larger balances from phishing attacks and online threats.

- Avoid Connecting Main Wallets to Unknown Platforms

Connecting a primary wallet to unfamiliar websites or DeFi applications can increase security risks. Using a separate wallet for testing new platforms can help protect long-term holdings.

- Enable Two-Factor Authentication

Two-factor authentication adds an extra layer of protection for exchange accounts and related services. It can help reduce the risk of unauthorized account access.

- Review Wallet Permissions Regularly

Some wallet approvals remain active long after a transaction is completed. Regularly reviewing permissions can help identify and remove unnecessary smart contract access.

- Store Recovery Phrases Offline

Recovery phrases should never be stored in screenshots, cloud storage, or messaging apps. Keeping them securely offline helps reduce the risk of unauthorized wallet access.

- Safer Wallet Management Starts With Good Habits

Using multiple wallets is common in crypto and does not automatically indicate suspicious activity. The most important factor is understanding how each wallet is used and maintaining strong crypto wallet safety practices over time.

Using multiple wallets is common in crypto and does not automatically indicate suspicious activity. In many cases, separating wallets actually improves organization and reduces risk when combined with good crypto wallet safety habits. Understanding wallet types, storage methods, and permission management plays an important role in long-term security, especially when choosing a safe crypto wallet for storing larger balances.

Understanding the Difference Between Smart Wallet Management and Suspicious Transfers

Having more than one crypto wallet is quite common among many people who invest their money in cryptocurrencies. Indeed, the traders, the investors, the DeFi participants, and even the companies have their own reason to keep the cryptocurrency in multiple wallets.

However, Capx Recovery, a well-known firm engaged in blockchain investigation, always has cases where the scammers quickly transfer the illegally obtained cryptocurrencies from one wallet to another in order to avoid blockchain tracking and confusion regarding the destination of the funds.

The key difference is usually the context behind the transfers. Legitimate wallet activity is typically expected and authorized, while scam-related movement often appears sudden, unexplained, or connected to withdrawal problems and unauthorized transactions.

As crypto scams continue evolving, understanding these patterns can help users recognize warning signs earlier and respond faster when something feels wrong. For individuals dealing with suspicious wallet activity or potential withdrawal scams, seeking professional help for blockchain investigation or crypto tracing support may help provide greater clarity into how the funds were moved and what steps can be taken next.If you believe you may have been targeted by a crypto investment scam or need assistance with blockchain tracing and investigation, contact us to learn how our team can help assess your case and guide you through the next steps.

FAQs

Is moving crypto through multiple wallets always suspicious?

No. Moving crypto across multiple wallets is very common and often part of normal blockchain activity. Exchanges, businesses, and individual users regularly transfer funds between wallets for security, operational, or privacy reasons. The concern usually begins when transfers are unexpected, unauthorized, or connected to withdrawal issues.

Why do scammers transfer stolen crypto between different wallets?

Scammers often move stolen funds across multiple wallet addresses to make blockchain tracing more difficult. Rapid transfers, wallet hopping, and splitting funds into smaller transactions can help obscure transaction trails and delay investigations into where the crypto was ultimately sent.

Can stolen crypto still be traced after it moves across multiple wallets?

In many cases, yes. Because blockchain transactions are publicly recorded, investigators can often follow transaction histories across wallet addresses. While scammers may attempt to hide fund movements using multiple transfers, blockchain tracing tools can still identify patterns, connected wallets, exchange deposits, and other transaction activity.

What should I do if my crypto was transferred without permission?

If you notice unauthorized wallet activity, stop interacting with suspicious platforms immediately and save all transaction details, wallet addresses, screenshots, and communication records. Reviewing wallet permissions, revoking suspicious smart contract access, and seeking professional blockchain investigation support early may help preserve important evidence and clarify how the funds were moved.